Investment

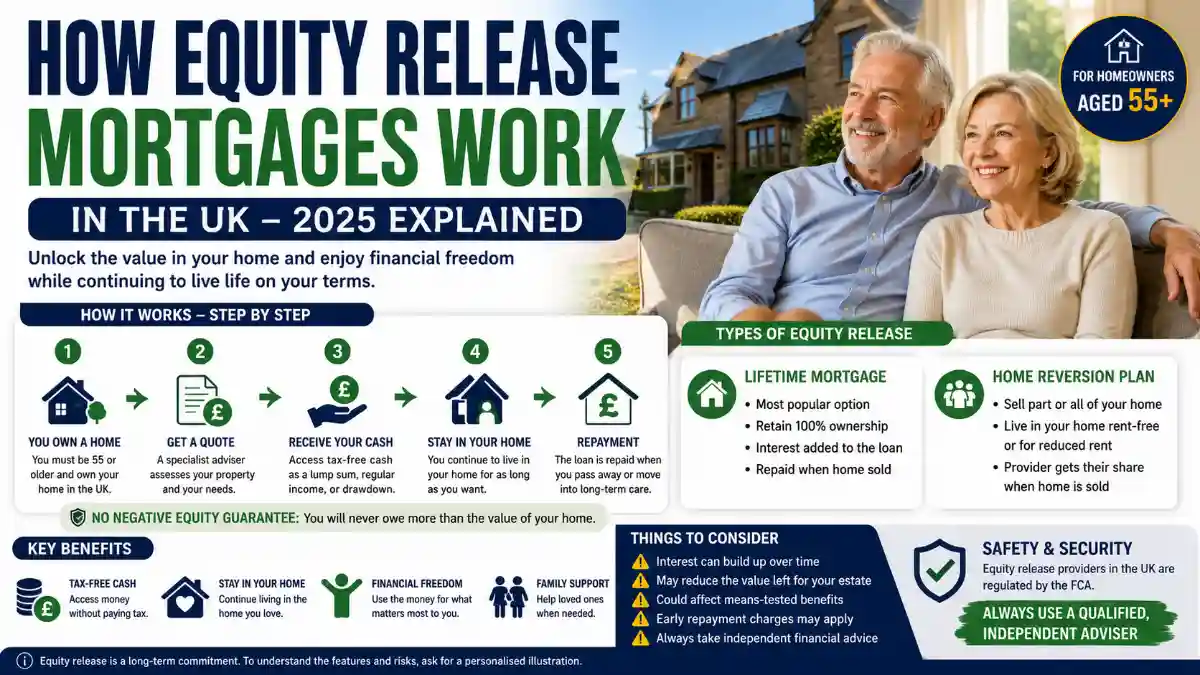

How Equity Release Mortgages Work in the UK – 2025 Explained

Equity release mortgages have become one of the most popular retirement finance options for homeowners in the UK. In 2025, rising living costs, increasing energy bills, healthcare expenses, and longer life expectancy are encouraging many people over the age of 55 to look for additional financial support during retirement.

For many retirees, their home is their biggest financial asset. However, while property values may be high, cash flow during retirement can often be limited. Equity release mortgages provide a solution by allowing homeowners to unlock money tied up in their property without needing to sell their home immediately.

This financial option can help retirees improve their lifestyle, cover expenses, support family members, pay off debts, or fund home improvements while continuing to live in their property.

However, equity release is a major long-term financial decision. Understanding how it works, the different types available, costs, risks, and repayment structure is extremely important before choosing any plan.

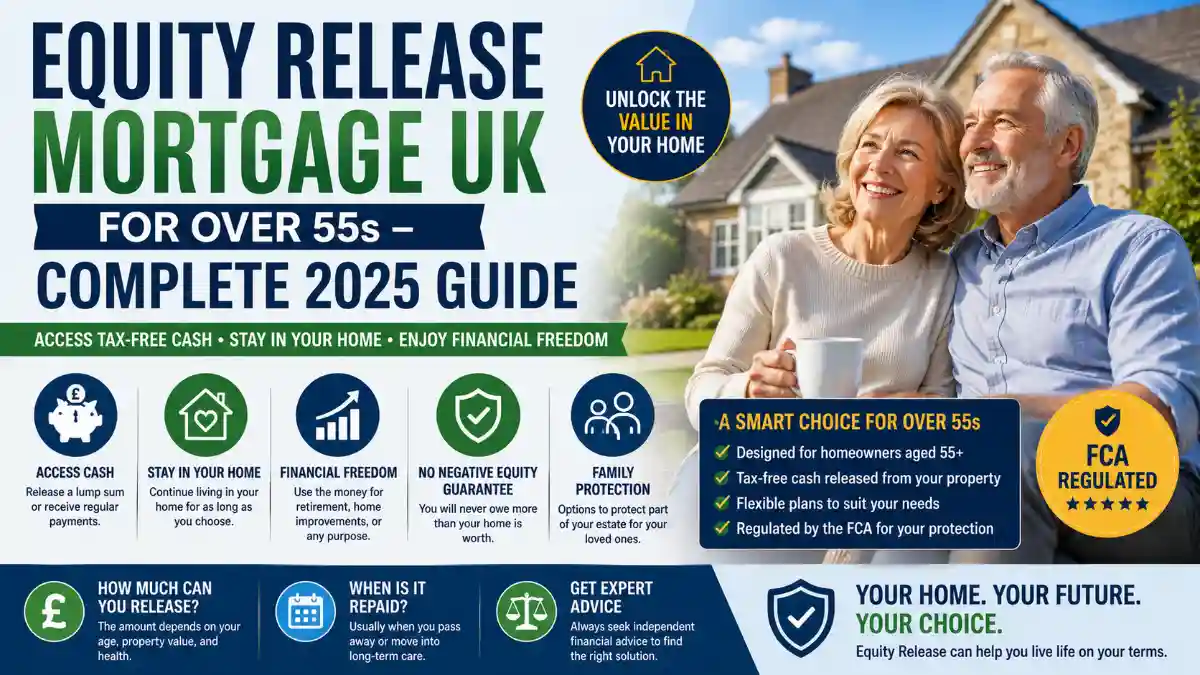

This complete guide explains how equity release mortgages work in the UK in 2025, including eligibility, benefits, disadvantages, repayment methods, and expert advice for homeowners.

What Is an Equity Release Mortgage?

An equity release mortgage allows homeowners aged 55 or older to borrow money against the value of their home while continuing to live there.

Instead of selling the property, homeowners can access tax-free cash from their property value.

The money released can be taken as:

- A lump sum

- Regular monthly income

- Flexible withdrawals over time

The loan is usually repaid later through the sale of the property after the homeowner passes away or moves permanently into long-term care.

Why Equity Release Is Growing in Popularity

Several factors are driving demand for equity release mortgages in 2025:

- Rising retirement living costs

- Limited pension income

- Higher property values

- Longer retirement periods

- Desire to stay in family homes

- Increased financial flexibility needs

Many UK homeowners are “property rich but cash poor,” meaning they own valuable homes but have limited retirement income.

Equity release helps convert property wealth into usable cash.

Main Types of Equity Release Mortgages

There are two primary forms of equity release available in the UK.

1. Lifetime Mortgage

A lifetime mortgage is the most common type of equity release product in the UK.

With this option:

- You retain ownership of your home

- You borrow money against the property value

- Interest is added over time

- Repayment happens when the property is eventually sold

Key Features

- Fixed or variable interest rates

- No required monthly repayments in many plans

- Flexible withdrawal options

- Tax-free cash access

The loan amount depends on:

- Your age

- Property value

- Health condition

- Lender rules

Older applicants may qualify for larger amounts.

2. Home Reversion Plan

A home reversion plan works differently.

Under this arrangement:

- You sell part or all of your property to a provider

- You continue living in the property

- The provider receives their share when the home is sold later

This type is less common than lifetime mortgages in 2025.

Who Can Apply for Equity Release?

Basic eligibility requirements generally include:

- Minimum age of 55

- UK residential property ownership

- Main home residence

- Property meeting lender standards

Lenders may also evaluate:

- Property condition

- Property value

- Remaining mortgage balance

Higher-value homes often qualify for larger release amounts.

How Much Equity Can You Release?

The amount available depends on several factors:

- Your age

- Property value

- Health condition

- Type of plan

- Interest rates

In general:

- Older homeowners can borrow more

- More valuable properties increase borrowing potential

Some providers also offer enhanced plans for people with certain medical conditions or lifestyle factors.

How Interest Works on Equity Release Mortgages

Interest is one of the most important factors to understand.

With many lifetime mortgages:

- Interest compounds over time

- Interest is added to the original loan

- The total debt can grow significantly over many years

For example:

- Borrowed money plus accumulated interest is repaid when the property is sold later.

Some modern plans now allow optional interest payments to reduce future debt growth.

Ways to Receive the Money

Equity release funds can usually be received in different ways.

Lump Sum

You receive the full amount at once.

Suitable for:

- Large expenses

- Debt repayment

- Major home renovations

Drawdown Facility

You withdraw smaller amounts over time.

Benefits include:

- Interest applies only to withdrawn money

- Better long-term cost control

- Flexible access to funds

Drawdown plans are becoming increasingly popular in 2025.

Regular Income Option

Some plans provide regular monthly payments to support retirement income.

Advantages of Equity Release Mortgages

1. Stay in Your Home

One of the biggest advantages is continuing to live in your property.

This allows retirees to remain in familiar surroundings without needing to downsize.

2. Tax-Free Cash Access

Money released through equity release is usually tax-free.

This can provide significant retirement financial support.

3. No Mandatory Monthly Repayments

Many plans do not require monthly repayments, reducing financial pressure during retirement.

4. Flexible Financial Freedom

The money can be used for:

- Retirement lifestyle improvements

- Travel

- Medical costs

- Home improvements

- Supporting family

- Debt repayment

5. Modern Consumer Protections

Most regulated providers now offer:

- No negative equity guarantee

- Flexible repayment options

- Inheritance protection features

Risks and Disadvantages

Although equity release offers many benefits, there are also important risks.

1. Reduced Inheritance

The loan and accumulated interest reduce the property value left for beneficiaries.

2. Compound Interest Growth

Interest can increase rapidly over time if repayments are not made.

This can significantly increase the total debt.

3. Impact on Government Benefits

Large cash releases may affect eligibility for certain means-tested benefits.

4. Early Repayment Charges

Some plans include penalties for early repayment.

Understanding contract details carefully is extremely important.

5. Property Market Risks

Future housing market conditions may affect long-term outcomes.

No Negative Equity Guarantee

One important modern feature is the no negative equity guarantee.

This ensures:

- You or your family will never owe more than the property value

This protection has become standard among regulated UK providers.

Equity Release and Existing Mortgages

If you still have a traditional mortgage:

- Part of the released funds may need to repay the existing mortgage first.

Remaining money becomes available afterward.

Costs and Fees Involved

Potential costs may include:

- Adviser fees

- Legal fees

- Property valuation fees

- Arrangement fees

- Interest charges

Comparing providers carefully helps reduce long-term costs.

Importance of FCA Regulation

In the UK, equity release products are regulated by the Financial Conduct Authority (FCA).

Always choose:

- FCA-authorized lenders

- Qualified financial advisers

- Regulated legal professionals

This improves safety and consumer protection.

Why Independent Financial Advice Matters

Equity release is a major long-term financial decision.

Professional advisers help evaluate:

- Suitability

- Risks

- Alternatives

- Tax implications

- Family impact

Independent advice is strongly recommended before signing any agreement.

Alternatives to Equity Release

Before choosing equity release, homeowners should also consider alternatives such as:

- Downsizing

- Pension withdrawals

- Savings usage

- Remortgaging

- Family support

- Part-time retirement work

Different retirement situations require different financial solutions.

Common Mistakes to Avoid

Releasing More Money Than Necessary

Borrowing too much increases future interest costs.

Ignoring Family Discussions

Open conversations with family members help avoid future misunderstandings.

Not Comparing Providers

Interest rates and product features vary significantly.

Choosing Plans Without Advice

Professional guidance is essential for major retirement decisions.

Future of Equity Release in the UK

The UK equity release market continues growing rapidly.

Key future trends include:

- More flexible repayment options

- Lower interest competition

- Digital application systems

- Improved retirement planning tools

- Better consumer protections

As property wealth continues increasing, equity release may become an even more important retirement finance solution.

Conclusion

Equity release mortgages in the UK provide homeowners over 55 with a way to unlock property wealth while continuing to live in their homes. In 2025, these products are becoming more flexible, safer, and more popular as retirees seek additional financial support.

However, equity release is a long-term commitment that affects inheritance, future finances, and retirement planning. Understanding how the process works, the interest structure, risks, and repayment terms is extremely important before making a decision.

For many retirees, equity release can provide financial freedom, lifestyle improvements, and peace of mind during retirement. But careful planning, comparing providers, and seeking professional financial advice remain essential for choosing the right solution.

-

Investment12 hours ago

Investment12 hours agoDrive Any Vehicle Home with Zero Down Payment in 2026

-

automobile21 hours ago

automobile21 hours agoTruck Accident Insurance Claim Process: Step-by-Step Complete Guide

-

Traffic Rules21 hours ago

Traffic Rules21 hours agoNew Traffic Rules in 2026 Every Driver Must Know

-

Investment12 hours ago

Investment12 hours ago0 Down Payment Car Finance Offers You Shouldn’t Miss

-

Latest News13 hours ago

Latest News13 hours agoInheritance Tax Planning Strategies in the UK (2026 Ultimate Guide)

-

Investment13 hours ago

Investment13 hours agoUltimate Wealth Management Guide 2026 for USA & India Investors

-

Construction21 hours ago

Construction21 hours agoBig Construction Projects and Their Impact on Employment

-

Investment12 hours ago

Investment12 hours agoBuy a Car with 0 Down Payment – Easy Finance Guide 2026